TCTM— To help businesses accurately and justifiably price elevator maintenance services and to allow building operation managers to allocate budgets more effectively, the Vietnam Elevator Association (VNEA) has recently released a Cost Estimation Table for Elevator Maintenance. This table is based on TCCS 02:2024/VNEA regarding labour norms and Circular No. 11/2021/TT-BXD issued by the Ministry of Construction.

To ensure the safety and longevity of construction works during use, as stipulated by regulations, the Ministry of Construction issued Circular No. 11/2021/TT-BXD, which provides guidelines on determining maintenance costs for construction projects. Elevators, being a critical component of any building, must also be maintained by the principles outlined in this circular.

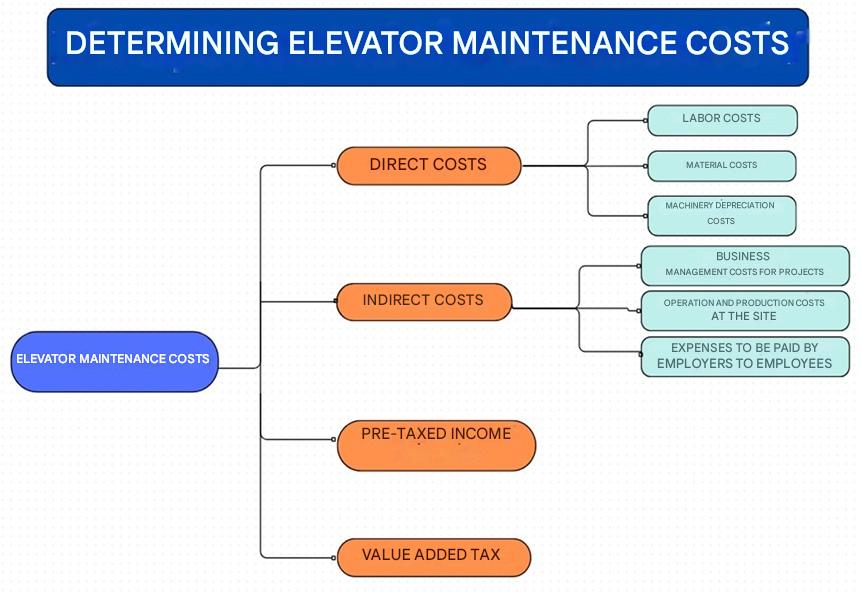

According to Circular No. 11/2021/TT-BXD on the guidance for determining and managing construction investment costs, a cost estimate must include direct costs, indirect costs, pre-taxable income, and value-added tax (VAT).

However, for an accurate maintenance cost estimate, clear labour norms are essential. Until recently, the lack of specialized labour norm guidelines for the elevator industry had made it difficult for both building managers and regulatory agencies to develop and approve appropriate budgets for elevator maintenance and repair activities.

Meanwhile, elevator maintenance prices vary widely between providers, from several hundred thousand VND per visit to several million, highlighting the need for standardized costing.

To address this, TCCS 02:2024/VNEA on labour norms for elevator maintenance and repair sets out specific benchmarks for each task, required time, and personnel standards involved.

This article provides a detailed breakdown of how to determine maintenance costs based on TCCS 02:2024/VNEA and Circular No. 11/2021/TT-BXD, issued on August 31, 2021, as follows:

1. Direct costs:

– Labour costs for executing maintenance tasks such as periodic inspections, regular repairs, and emergency standby services;

– Costs of consumable materials used in these tasks;

– Depreciation of maintenance equipment and tools.

2. Indirect costs:

These refer to expenses incurred during construction, project management, and other investment-related activities, often categorized as overheads. They include:

– Business management expenses allocated to the project;

– On-site operational expenses related to maintenance activities;

– Statutory employer contributions for employees (e.g., insurance, union fees, etc.).

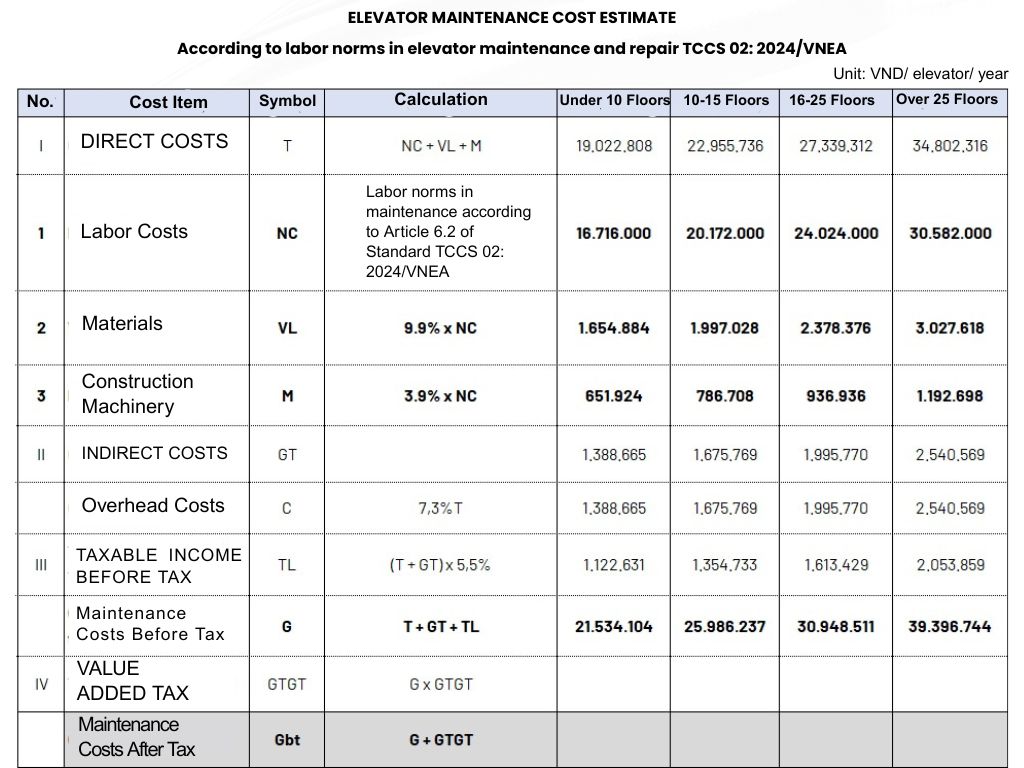

As per Circular No. 11/2021/TT-BXD, the overhead cost for maintaining civil construction projects is set at 7.3% of direct costs.

3. Pre-Taxable Income: This represents the profit margin—the difference between the selling price and the production cost of the service. It is calculated as a percentage of both direct and indirect costs.

Under Circular No. 11/2021/TT-BXD, the pre-taxable income is set at 5.5% of the total direct cost, commonly called the “normative profit.”

4. Value-Added Tax (VAT): According to Resolution 174/2024/QH15, the VAT will continue to be reduced by 2% in the first half of 2025.

According to Circular No. 11/2021/TT-BXD on Guidelines for Calculating Maintenance Costs for Construction Works, elevator maintenance costs are primarily determined based on direct costs. Specifically:

– The major portion of elevator maintenance expenses is allocated to labour costs, which cover the wages of technicians. Based on TCCS 02:2024/VNEA—Labour Norms for Elevator Maintenance and Repair, labour cost estimates can be calculated for each project, varying depending on the number of floors served by the elevator being maintained.

– An important component of maintenance costs is consumable materials, for which no fixed norm currently exists. In this cost model, the material cost is estimated based on practical data from several companies. On average, material expenses account for 9.9% of the defined labour cost.

– Similarly, equipment depreciation and usage costs for maintenance activities are estimated at 3.9% of the labour cost, based on real-world data from elevator service providers.

Based on the above analysis, the following reference table can be used to estimate elevator maintenance costs. This table not only supports professional elevator maintenance units in calculating service unit prices and organising operational structures, but is also particularly valuable for building management units in budgeting and allocating funds for elevator maintenance under their authority.

Important Notes:

– Applicable to buildings implementing monthly periodic maintenance. Details of the work scope, time requirements, and personnel standards follow Sections 6.1 and 6.2, Article 6 of the Labour Norms in Elevator Maintenance and Repair—TCCS 02:2024/VNEA.

– The cost table does not include expenses for replacing parts, components, or materials required for actual breakdown repairs or wear and tear.

– Cost categories, overhead cost ratios, and pre-tax income margins are applied by Appendix III—Method for Determining Construction Costs, issued with Circular No. 11/2021/TT-BXD dated August 31, 2021, by the Ministry of Construction.

For full reference: Access TCCS 02:2024/VNEA—Labour Norms in Elevator Maintenance and Repair here.